SPECIAL REPORTS AND PROJECTS

Agribusiness and big finance’s dirty alliance is anything but “green”

Just prior to Amaggi’s green bond, Brazil’s biggest producer of soybeans, SLC Agrícola, issued its own USD 95 million green bond for what it calls “regenerative agriculture”. SLC’s farms cover 460,000 hectares of land, mainly in the Cerrado,where it has deforested at least 30,000 hectares of native vegetation and where it has been fined several times by Brazil’s federal environmental agency for its activities.4

But the big financial companies want the public to bear the risks for their ventures. Green finance may be promoted by private financial companies but it depends heavily on governments. Only governments can generate demand by implementing laws and policies that force companies to make “green” investments, often in the form of taxes on carbon that are passed on to consumers and that disproportionately penalise the poorest.

One of the fastest growing instruments of green finance, “sustainability-linked” bonds (SLB) and bank loans, takes these weaknesses to an extreme. These bonds and loans are issued without specifying which projects the proceeds are destined for or what the social and environmental benefits will be.

To make this happen, agribusiness companies are working aggressively with corporations from other sectors and corporate-dominated spaces like the Food and Land Use Coalition, the World Economic Forum and The Food Systems Summit to push for so-called “nature-based solutions” with an emphasis on land use and the agricultural sector.27

|

Company

|

Green finance mechanism

|

Notes

|

|

Green bond worth USD 94 million issued in 2020. It was raised in green agribusiness bonds (Agribusiness Receivables Certificates) to be applied in digital and low Carbon Farming Practices, Integrated Systems (Crop-Livestock) in its 460 thousand hectares of soy, maize and cotton monoculture plantations. The green bond was issued through Bradesco bbi, Itaú and Santander banks.

|

The second party opinion (SPO), Resultante, listed in its report several passages linking SLC Agricola with environmental crimes and land grabbing. Although it was approved, the issuance of the green bond was validated with the recommendation of not allocating the funds to those questionable areas.

|

|

|

Sustainability bond worth USD 750 million in 2021 to be applied to its 170 thousand hectares in a mix of environment projects such as renewable energy and land use, as well as in socio-economic activities as job creation. The bond was coordinated by BNP Paribas, Bradesco Securities, Inc., Citigroup Global Markets, Inc., Itaú BBA USA Securities, Inc., JP Morgan Chase & Co., Rabobank and Santander Investment.

|

Amaggi group is the largest exporter of soybean from Brazil and is a major buyer of soybean from known deforesters like SLC Agrícola and BrasilAgro, and has not yet agreedto a 2020 cut-off date for land clearing in the Cerrado region.

|

|

|

Green bond of EUR 75 million (USD 89 million). to be issued in Europe in 2021. Proceeds will be used for various activities including reducing greenhouse gas emissions and expanding its farming operations.

|

AgriNurture Inc. is a company based in the Philippines that received early backing from Cargill’s hedge fund Black River and the Far Eastern Agricultural Investment Company of Saudi Arabia. It has become one of the largest farming companies and agricultural exporters in the country through the development of large-scale farms and plantations, most recently for maize in Mindanao.

|

|

|

Olam has secured three “green” loan facilities since 2018 from different consortiums of banks: a sustainability-linked loan of USD 500 million in 2018, a USD 525 million sustainability-linked revolving credit facility in 2019 and a USD 525 million sustainability loan in 2020– all to be used for general spending but with an interest margin dependent on Olam’s ability to meet various targets. In 2019 it launched the world’s first “digital loan” of USD 350 million.

|

Olam is an Indian non-resident company based in Singapore. It is one of the world’s largest commodity traders and has invested heavily in farming operations and contract farming schemes, particularly in Africa and Latin America. It is part-owned by Singapore’s sovereign wealth fund Temasek and Japan’s Mitsubishi. It claims to have 2.4 million hectares under direct management, including a controversial 144,000 hectare oil palm plantation concession in Gabon.

|

|

|

Sustainability-linked loan with 20 banks, worth USD 2.3 billion in 2019. ING, BBVA and Rabobank acted as sustainability coordinators. ABN AMRO has acted as coordinator and facility agent.

|

It was the largest loan by an agricultural trader. The loan is linked to a general year-on-year improvement target of ESG performance, assessed by SPO Sustainalytics and increasing its traceability of Brazilian agri-commodities. In late 2020, the World Bank’s International Financing Corporation (IFC) began subsidising the traceability of the direct suppliers of soybean in Matopiba, in the Cerrado region (Brazil).

|

|

|

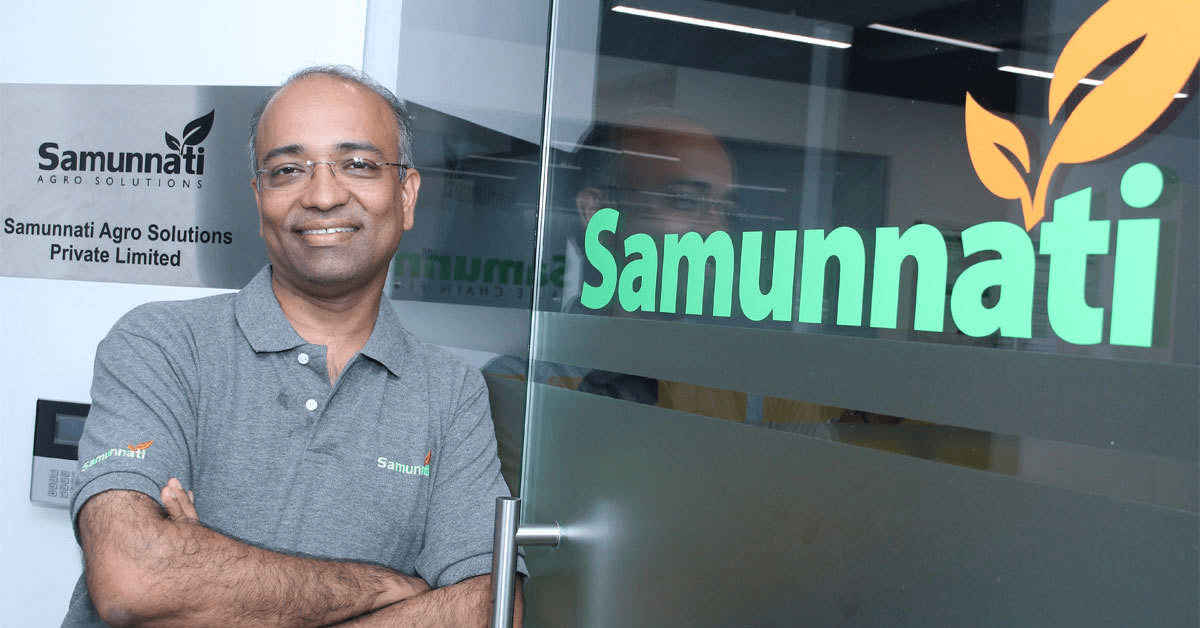

In July 2021, Samunnati issued a USD 4.6 million agricultural green bond via the market platform Symbiotics. The proceeds are to be “fully allocated towards climate smart agriculture.”

|

Samunnati is an Indian micro-credit lender for farmers and agribusiness. Its investors include the US pension fund TIAA and the US government’s International Development Finance Corporation.

|

|

|

A ten-year loan of USD 50 million to soybean suppliers in Cerrado to support a deforestation-free target. This is Santander Bank and The Nature Conservancy (“TNC”) financial mechanism that is not formally considered as green finance, but that links the expansion of soy to a “compliance with environmental law” in Brazil.

|

The Responsible Commodities Facility (RCF) and the Soft Commodities Forum Platform, bring together giant agribusiness traders (ABCD, Cofco, Viterra -ex Glencore Agriculture) to issue new “green” agribusiness debt instruments for the expansion of soybean plantations over pasture areas.

|

|

|

Cargill

|

Land Innovation Fund, created with Cargill’s USD 30 million to support the expansion of soybean over degraded pasture areas in Argentina and Paraguay’s Cerrado and Grand Chaco. The fund is incorporating the suppliers into a traceability chain for measuring soil carbon emissions. The Bank of Cargill is increasing its use of agribusiness bonds to fund soybean suppliers, with a rise of 30% in 2020 in Agribusiness Letters of Credit. The company is part of the Brazilian Initiative

for Green Finance to support the emission of green bonds in agriculture.

|

Cargill is perhaps the soybean trader most linked to deforestation and fires in their supply chain. In 2019, Nestlé stopped sourcing all of its purchases of Brazilian soy from Cargill with the trader not being able to trace soybeans from its suppliers. In 2020, Norwegian Grieg Seafood did not allow any funds from its Green Bond worth USD 103 million to be used to purchase feed supply from Cargill until the company had significantly reduced itsrisk of soybean-related deforestation in Brazil.

|

|

Onesustainable transition bond worth USD 500 million issued in 2019 through BNP Paribas, ING and Santander, to purchase deforestation-free cattle from direct suppliers in Amazonia.

Onesustainability-linked loan worth USD 30 million in 2021 as part of green financing to support Mafrig’s transition to a no-deforestation requirement across its entire chain.

|

The first labelled “transition bond” issued in the world, after the green bonds held by one of the world’s biggest beef producers were refused by investors. The bond was re-labelled to support high-emitting companies that do not fit green bonds requirements to clean up their supply chain. Only two other transition bonds of this kind were issued in 2020 due to the lack of reliability.

|

|

|

Green bond worth USD 5 million issued as a green agribusiness bond (Agribusiness Receivables Certificates) to support the expansion of regenerative and organic agriculture production in its 1200 hectares located in São Paulo, Brazil. It was structured by the financial consultancy Ecoagro.

|

The first certified agriculture green bond issued in the world, according to the new CBI principles for the agriculture sector. According to Rizoma’s founding partner, Pedro Paulo Diniz, regenerative agriculture has the potential to offset “more than 100% of human carbon emissions” and often “has more biodiversity than a native forest”.

|

|

|

Ventisqueros

|

Chilean salmon farmer Ventisqueros announced at the end of 2020 that it had landed a USD 120 million green loan from banks Rabobank and DNB. The proceeds will fund the expansion of production from the current 40,000 metric tonnes to 60,000 metric tonnes.

|

In 2019, there was a massive escape of salmon from one of Ventisqueros’ farms in Chiloé leading to a complaint from the National Fisheries and Aquaculture Service (Sernapesca) before the Superintendency of the Environment and in court. The company has also refused to comply with a sentence issued by the Council for Transparency ordering them to provide Oceana with data on their use of antibiotics in 2015, 2016 and 2017.

|

|

Mowi

|

Mowi completed a USD 165 million green bond in 2020, the first green bond issued by a seafood company. The proceeds will be used for green projects as defined by Mowi’s green bond framework.

|

Norway-based Mowi is the world’s largest aquaculture company and largest salmon producer. It is notorious for the aggressive tactics it deploys against critics and for the damage it has caused to the environment, particularly to wild salmon stocks.

|

|

Long-term loan for the recovery of degraded pasture areas by soybean planting via the Reverte programme, led by Syngenta in partnership with TNC and Itaú bank. Although not formally a “green loan”, the Itaú bank already reserved USD 86 million to “restore” 30 thousands hectares in Cerrado with soybean and other inputs provided by Syngenta.

|

The Reverte programme announced by Syngenta aims to “restore” 1 million hectares by 2025. In addition to using green finance to sell inputs and the obligation to use the traceability system, the Syngenta Group traded the seeds in exchange for the soybean harvest (barter operation) and operated the export of the company’s first cargo ship of soybeans from Brazil to China.

|

|

|

Three Green bonds totalling USD 639 million in 2020 and 2021 coordinated by Morgan Stanley to produce ethanol from maize and produce 100% renewable energy.

One sustainability-linked bond worth USD 26 million with Credit Suisse Bank and one sustainability-linked loan of USD 33 million in 2020 with Santander bank, conditioned to: reducing the carbon footprint; improving the traceability of suppliers, and disclosure and transparency in its annual reports.

|

This was the first green agribusiness bond for the bioenergy sector, called Agribusiness Receivable Certificates (CRA). The company produced 100% of ethanol for maize. The bioenergy sector, along with the forestry sector, is one of the biggest issuers of green and sustainability bonds.

|

|

|

Suzano S.A.

|

Four Green bonds since 2016 totalling USD 1.6 billion for pulp and paper industrial forestry. The offering was coordinated by J.P. Morgan, Goldman Sachs, Morgan Stanley, Bank of America, BNP, Crédit Agricole, MUFG, Santander, Rabobank, SMBC Nikko, Scotiabank and Mizuho.

Two sustainability-linked bonds (SLB) totalling USD 1.2 billion in 2020 and another USD1 billion SLB issued in June 2021, through BNP Paribas, BofA, J.P. Morgan, Mizuho, Rabo Securities and Scotiabank.

Onesustainability-linked loan worth USD 1.6 billion in January 2021 operated by BNP Paribas.

Both SL bonds and loans are linked to reducing the company’s direct emissions and water consumption across all its operations and purchases (scopes 1 and 2) and also have an “inclusion” target to have woman in leadership positions.

|

Suzano was the first issuer of green bonds and sustainability-linked bonds in Brazil and has 37% of its debts tied to green finance. Suzano S.A has more than 1 million hectares of industrial pine and eucalyptus monoculture plantations in Brazil and is historically linked to a series of human rights violations against local communities and the labour rights of its workers.

|

|

Sustainability bond worth USD 95 million issued in 2018 by the USAID initiative Tropical Landscapes Financing Facility (TLFF) through BNP Paribas in partnership with WWF. The bond was issued to fund 88 thousand hectares of rubber plantation for PT Royal Lestari Utama (RLU), an Indonesian joint venture between France’s Michelin and Indonesia’s Barito Pacific Group.

|

Asia’s first sustainability debt instrumentand part of the Memorandum of Understanding between UN Environment and BNP Paribas that was signed at the One Planet Summit in Paris in December 2017. The target is to reach USD 10 billion of innovative sustainable finance by 2025 for projects that support sustainable agriculture and forestry in ways that help solve the climate crisis.

|

Related posts:

The global farmland grab goes green

The global farmland grab goes green

World Bank branch indirectly backs coal megaproject despite green pledge

World Bank branch indirectly backs coal megaproject despite green pledge

International Finance Corporation Should Stop Bankrolling Destructive Agribusiness

International Finance Corporation Should Stop Bankrolling Destructive Agribusiness

EBRD launches new agribusiness strategy

EBRD launches new agribusiness strategy

SPECIAL REPORTS AND PROJECTS

‘Food and fossil fuel production causing $5bn of environmental damage an hour’

Related posts:

Activists storm TotalEnergies’ office ahead of G20 Summit, demand end to fossil fuel expansion in Africa

Activists storm TotalEnergies’ office ahead of G20 Summit, demand end to fossil fuel expansion in Africa

New billion-dollar loans to fossil fuel companies from SEB, Nordea and Danske Bank.

New billion-dollar loans to fossil fuel companies from SEB, Nordea and Danske Bank.

Fossil fuel opponents lobby Africans for support

Fossil fuel opponents lobby Africans for support

Ecological land grab: food vs fuel vs forests

Ecological land grab: food vs fuel vs forests

SPECIAL REPORTS AND PROJECTS

Britain, Netherlands withdraw $2.2 billion backing for Total-led Mozambique LNG

Related posts:

Uganda, Total sign crude oil pipeline deal

Uganda, Total sign crude oil pipeline deal

Witness Radio – Uganda, Community members from Mozambique and other organizations around the world say NO to more industrial tree plantations

Witness Radio – Uganda, Community members from Mozambique and other organizations around the world say NO to more industrial tree plantations

NGOs file suit against Total over Uganda oil project

NGOs file suit against Total over Uganda oil project

Agribusiness Company with financial support from UK, US and Netherlands is dispossessing thousands.

Agribusiness Company with financial support from UK, US and Netherlands is dispossessing thousands.

SPECIAL REPORTS AND PROJECTS

The secretive cabal of US polluters that is rewriting the EU’s human rights and climate law

Leaked documents reveal how a secretive alliance of eleven large multinational enterprises has worked to tear down the EU’s flagship human rights and climate law, the Corporate Sustainability Due Diligence Directive (CSDDD). The mostly US-based coalition, which calls itself the Competitiveness Roundtable, has targeted all EU institutions, governments in Europe’s capitals, as well as the Trump administration and other non-EU governments to serve its own interests. With European lawmakers soon moving ahead to completely dilute the CSDDD at the expense of human rights and the climate, this research exposes the fragility of Europe’s democracy.

Key findings

- Leaked documents reveal how a secretive alliance of eleven companies, including Chevron, ExxonMobil, and Koch, Inc., has worked under the guise of a “Competitiveness Roundtable” to get the Corporate Sustainability Due Diligence Directive (CSDDD) either scrapped or massively diluted.

- The companies, most of which are headquartered in the US and operate in the fossil fuel sector, aimed to “divide and conquer in the Council”, sideline “stubborn” European Commission departments, and push the European People’s Party (EPP) in the European Parliament “to side with the right-wing parties as much as possible”.

- Chevron and ExxonMobil were in charge of mobilising pressure against the CSDDD from non-EU countries. The Roundtable companies endeavoured to get the CSDDD high on the agenda of the US-EU trade negotiations and also worked on mobilising other countries against the CSDDD, in order to disguise the US influence.

- Roundtable companies paid the TEHA Group – a think tank – to write a research report and organise an event on EU competitiveness, which echoed the Roundtable’s position and cast doubt on the European Commission’s assessment of the economic impact of the CSDDD.

While Europeans were told that their governments were negotiating a landmark law to hold corporations accountable for human rights abuses and climate damage, a secretive alliance of US fossil fuel giants was working behind the scenes to destroy it. Collaborating under the innocent-sounding name ‘Competitiveness Roundtable’, eleven multinational enterprises have worked closely to eviscerate several EU sustainability laws, including the Corporate Sustainability Due Diligence Directive (CSDDD) and the Corporate Sustainability Reporting Directive (CSRD). This Competitiveness Roundtable may be unknown, but its members are a who’s-who of polluting, mainly US, multinationals, including Chevron, ExxonMobil, and Dow. The group seems to have run rings around all branches of the EU and the Trump administration to get what they want: scrapping, or at least hugely diluting, the CSDDD.

Leaked documents obtained by SOMO reveal how, under the pretext of the now-near-magical concept of ‘competitiveness’, these companies plotted to hijack democratically adopted EU laws and strip them of all meaningful provisions, including those on climate transition plans, civil liability, and the scope of supply chains. EU officials appear not to have known who they were up against. But the documents obtained by SOMO show a high level of organisation and strategising with a clear facilitator: Teneo, a US public relations and consultancy company.

The documents indicate that many of the companies involved wanted to stay hidden from view. After all, if it were widely known that a secretive group of mostly American fossil fuel companies like Chevron, ExxonMobil, and Koch, Inc. was working as a coordinated organisation to dilute an EU climate and human rights law, that might raise questions and serious concern among the public and the policymakers they were targeting. Many of the companies in the Roundtable have never publicly spoken out against the CSDDD.

Big Oil’s ‘Competitiveness Roundtable’

The Competitiveness Roundtable is dominated by fossil fuel companies, including three Big Oil companies (ExxonMobil, Chevron, TotalEnergies) and three other companies with activities in the oil and gas sector (Koch, Inc., Honeywell, and Baker Hughes). Other members are Nyrstar (minerals and metals, a subsidiary of Trafigura Group); Dow, Inc. (chemicals); Enterprise Mobility (car rentals); and JPMorgan Chase (finance).

Teneo, the Roundtable’s coordinator, has a track record(opens in new window) of working with fossil fuel companies, including Chevron, Shell, and Trafigura, and was hired by the government of Azerbaijan to handle public relations(opens in new window) when it hosted the COP29 climate conference.

In February 2025, the European Commission published the Omnibus I proposal(opens in new window), which aims to “simplify” several EU sustainability laws, including the CSDDD. The documents obtained by SOMO reveal that the Roundtable companies, which have been meeting weekly since at least March 2025, worked on deep interventions within each of the three EU institutions to get the Omnibus I package to align exactly with their views. The EU institutions are expected to reach a final agreement on Omnibus I by the end of 2025.

The documents reveal that the Roundtable companies’ activities in the Parliament are far more significant than what is visible in the EU Transparency Register(opens in new window). Eight of the Roundtable’s lobbying meetings during the Strasbourg plenary sessions of May and June 2025, listed in the Transparency Register, show Teneo as the only attendee, thereby failing to disclose the names of other Roundtable companies that participated in these meetings. Another three meetings the Roundtable held were not found in the EU Transparency Register(opens in new window) at all.

“Divide and conquer” the Council

In the European Council, the Roundtable plotted to “divide and conquer” EU governments to get the climate article in the CSDDD deleted. In June 2025, during the final weeks of negotiations in the Council on the Omnibus I proposal, the Roundtable discussed lobbying EU government leaders to “intervene politically” to ensure its priorities were included in the Council’s negotiation mandate. Subsequently, German Chancellor Merz and French President Macron reportedly(opens in new window) personally intervened(opens in new window) in the Council’s political process, leading to a dramatic dilution(opens in new window) of the texts(opens in new window) negotiated in the months before the intervention. Several of the changes made to the texts strongly align with the Roundtable’s demands, including delaying and substantially weakening the climate obligations, scrapping EU civil liability provisions, and limiting the responsibility of companies to take responsibility for their supply chains (the ‘Tier 1’ restriction).

Competitiveness Roundtable meeting document, 11 July 2025.

Additionally, the documents reveal that the Roundtable is still aiming to drum up a “blocking minority” to overturn the Council’s negotiation mandate during the trilogue negotiations, which started in November 2025. By “tak[ing] advantage of the ‘weak’ Council negotiating mandate” and disagreements between EU Member States on “contentious articles”, the Competitiveness Roundtable companies hope to force the Danish Council presidency to give up on including any form of climate obligations in the CSDDD – despite EU Member States’ agreement on this in the June 2025 Council mandate(opens in new window) .

To implement the divide-and-conquer strategy, the Roundtable assigned specific companies to “establish rapporteurships” with different EU governments. TotalEnergies would target the French, Belgian, and Danish governments, and ExxonMobil would target Germany, Hungary, the Czech Republic, and Romania.

Circumventing “stubborn” European Commission departments

The Roundtable also discussed working on “circumvent[ing]” two “stubborn” European Commission departments involved in the Omnibus political process, DG JUST and DG FISMA, which, in their view, were “unlikely to be willing to see our side of the story”. According to the documents, DG JUST opposed deleting the climate article and restricting the Directive’s scope to only very large enterprises. The Roundtable aimed to diminish the role of these departments by pressuring President Von der Leyen and Commissioners McGrath (DG JUST) and Albuquerque (DG FISMA) by “organising letters from Irish and German business groups” and using an event held by the European Roundtable for Industry to “target” Von der Leyen and McGrath.

Read full report: Somo.nl

Source: Somo

Related posts:

Victims of human rights violations in Uganda still waiting for redress

Victims of human rights violations in Uganda still waiting for redress

Business, UN, Govt & Civil Society urge EU to protect sustainability due diligence framework

Business, UN, Govt & Civil Society urge EU to protect sustainability due diligence framework

Development financiers fuel human rights abuses – New Report

Development financiers fuel human rights abuses – New Report

Global hunger falls, but millions in Africa still go without food, says UN

Wars are disrupting food systems, and ending world hunger requires urgent global action, experts say.

No Heritage Without its People: Why Ngorongoro Cannot be a World Heritage Site and an Eviction Zone

Campaigning LC I Chairpersons Barred from Land Transactions Until Polls End.

Peruvian communities have launched a global petition to halt a mining project they say threatens the water supply of over 10 million people.

‘Oil is a curse’: villages in Uganda face land ownership uncertainty

NEMA says it is restoring wetlands, but poor urban families say it is using the exercise to grab their land for new infrastructure projects – now they demand compensation and resettlement.

Ugandan farmers take TotalEnergies’ pipeline to UK court

Innovative Finance from Canada projects positive impact on local communities.

Over 5000 Indigenous Communities evicted in Kiryandongo District

Petition To Land Inquiry Commission Over Human Rights In Kiryandongo District

Invisible victims of Uganda Land Grabs

-

NGO WORK1 week ago

NGO WORK1 week agoRush: Global Scramble for Minerals Wages War on People and Planet

-

MEDIA FOR CHANGE NETWORK2 weeks ago

MEDIA FOR CHANGE NETWORK2 weeks agoNew MPs to undergo orientation on land governance

-

MEDIA FOR CHANGE NETWORK1 week ago

MEDIA FOR CHANGE NETWORK1 week agoMbale City Senior Lands Officer Charged with Abuse of Office Over Sale of Govt Property

-

MEDIA FOR CHANGE NETWORK2 weeks ago

MEDIA FOR CHANGE NETWORK2 weeks agoAfrican communities demand land rights amid mining expansion

-

MEDIA FOR CHANGE NETWORK1 week ago

MEDIA FOR CHANGE NETWORK1 week agoKibaale Residents Raise Corruption Concerns Over Delayed Land Title Processing

-

MEDIA FOR CHANGE NETWORK1 week ago

MEDIA FOR CHANGE NETWORK1 week agoCampaigning LC I Chairpersons Barred from Land Transactions Until Polls End.

-

NGO WORK5 days ago

NGO WORK5 days agoNo Heritage Without its People: Why Ngorongoro Cannot be a World Heritage Site and an Eviction Zone

-

MEDIA FOR CHANGE NETWORK2 days ago

MEDIA FOR CHANGE NETWORK2 days agoWars are disrupting food systems, and ending world hunger requires urgent global action, experts say.