ETC Group’s 2022 publication “Food Barons” exposed the increasing concentration of corporate power in the industrial food system.

1 It documented the rise of mergers and acquisitions, the increasing influence of finance capital, and the penetration of digitalisation and other disruptive technologies across corporate supply chains.

2During the Covid pandemic and the subsequent outbreak of war in Ukraine, these corporations showed how, during times of global shocks or crises, they could use their monopoly power to make obscene profits, with huge impacts on people the world over.

3Three years later, war persists in Ukraine and new wars and genocides are raging in Palestine, Sudan and the DR Congo. The US is pursuing a global trade war, global temperatures are smashing record highs, and diseases with pandemic potential (like bird flu) are still a cause of major disruptions.

4 The situation is as volatile as ever and, yet, corporate concentration in the food system has only continued unabated.

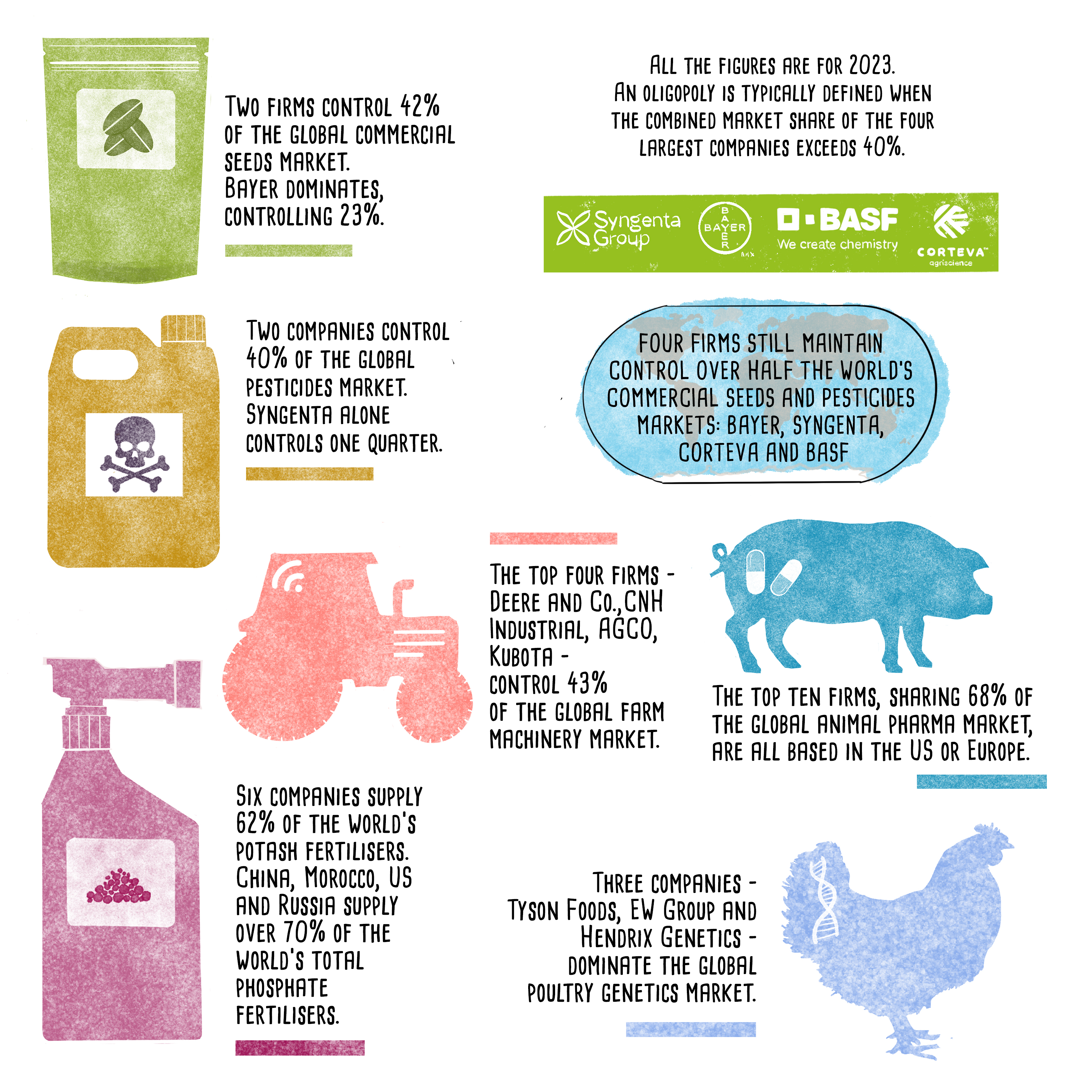

5In this report, we examine the state of corporate concentration in six sectors critical to agriculture: commercial seeds, pesticides, synthetic fertilisers, farm machinery, animal pharmaceuticals and livestock genetics. Corporate consolidation has increased in most of these sectors and four of them– seeds, pesticides, agricultural machinery and animal pharmaceuticals– meet the definition of an oligopoly, in which four companies control more than 40% of a market.

6 Concentration can be even higher at the national level, as is the case with synthetic fertilisers. In livestock genetics, where publicly available information is scarce, we focus on poultry – the largest sector within the meat industry – and its extreme and long-standing levels of corporate concentration.

This report also highlights corporate investment in new technologies, like digital platforms, artificial intelligence (AI) and gene editing, which are likely to deepen corporate power in the food system. It also looks at how they are buying up smaller companies in newly relevant sectors, and forging alliances with Big Tech companies and other corporations in the food sector to expand their dominance from seeds to supermarkets.

Concentration gives corporations more power to dictate prices and lobby policy makers. They can use this power to disrupt scientific research, block regulations that protect people’s health and the environment, and undermine democratic participation in the shaping of food systems. Concentration increases their ability to crush alternatives and ensure the expansion of a model of agriculture that is immensely profitable for them while being hugely destructive for people and the planet. The industrial food system is responsible for a third of global greenhouse gas emissions and it is the leading source of soil and water pollution and biodiversity loss. It destroys local food systems and economies, displaces peasants and indigenous peoples from their territories and forces them to migrate far from their homes. It is also built on the severe exploitation of workers.

Actions are urgently needed to take down the monopoly power of these corporations and to get power back into the hands of the world’s food producers, workers and consumers.

click on image for better resolution

Commercial seeds and pesticides

The commercial seed sector refers to crop seeds (primarily proprietary field crop and vegetable seeds) sold via the commercial market and genetically modified crop traits. Farmer-saved seed and seed supplied by governments and public institutions are not included.

The commercial seed sector refers to crop seeds (primarily proprietary field crop and vegetable seeds) sold via the commercial market and genetically modified crop traits. Farmer-saved seed and seed supplied by governments and public institutions are not included.The pesticides sector includes herbicides, insecticides and fungicides which are different types of agrochemical products that target weeds, insects and fungi, respectively.

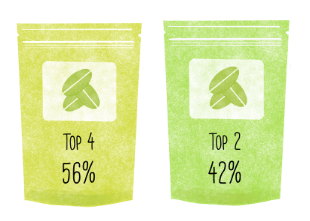

The slate of top companies in commercial seeds and pesticides are unchanged from 2022: BASF, Bayer, Corteva and Syngenta. They control 56% of the global seeds market (Bayer alone accounts for 23% of it), and 61% of the pesticides market (see Tables 1 and 2).

Compared to 2020, the revenues of these companies have increased significantly. But for Bayer all is not as well as it seems. Battered by an 80% decline in its share price since acquiring Monsanto in 2018, it initiated a restructuring in 2023, laying off about 7,000 employees to cut costs. Bayer’s financial problems are a result of multiple failures in court where juries have agreed with plaintiffs arguing that the company’s Roundup herbicide caused their cancers. It settled many claims in 2020 through a US$10.9 billion payout, but some 58,000 claims are pending. In April 2025, it was reported that Bayer might stop manufacturing glyphosate if it does not obtain court protection in the US against these lawsuits.

The seed corporations continue their focus on genetically modified crops, and have introduced some new varieties, such as Bayer’s shorter “smart” GM maize and BASF’s GM soybeans resistant to soybean cyst nematodes. They are also increasingly integrating artificial intelligence (AI) into their plant breeding. For example, Syngenta has a partnership with InstaDeep, a UK based company now acquired by the German biotechnology company BioNTech. The aim is to use AI technology to “learn the language of plant DNA” and make predictions on how different genetic sequences perform and how to alter their performance. Bayer claims that using AI to analyse genomic data has shortened breeding cycles from 5-6 years to only 4 months.

Table 1. Top 9 corporations in the commercial seeds sector

|

Ranking

|

Company (Headquarters)

|

Sales in 2023

(US$ millions)

|

% Global market share

|

|

1

|

Bayer (Germany)

|

11,613

|

23

|

|

2

|

Corteva (US)

|

9,472

|

19

|

|

3

|

Syngenta (China/Switzerland)

|

4,751

|

10

|

|

4

|

BASF (Germany)

|

2,122

|

4

|

|

|

Total top 4

|

27,958

|

56

|

|

5

|

Vilmorin & Cie (Groupe Limagrain) (France)

|

1,984

|

4

|

|

6

|

KWS (Germany)

|

1,815

|

4

|

|

7

|

DLF Seeds (Denmark)

|

838

|

2

|

|

8

|

Sakata Seeds (Japan)

|

649

|

1

|

|

9

|

Kaneko Seeds (Japan)

|

451

|

0.9

|

|

|

Total top 9

|

33,695

|

67

|

|

|

Total world market

|

50,000

|

100%

|

Another rapidly growing area of investment is biological pesticides and fertilisers. Biologicals (or bioinputs) describe a range of products derived from biological processes (as opposed to chemical synthesis), such as pesticides sprayed on crops or stimulants applied to soils to increase plant growth. But there is no standard definition, and regulations of these products are lax. According to industry estimates, the biologicals market is expected to grow to nearly US$22 billion by 2032, with an estimate of 1,200 companies engaged in the sector. All of the top pesticide companies are now heavily investing in it in order to ensure their dominance. Corteva, for example, recently bought up two biological manufacturers, Stoller and Symborg, while Syngenta signed a partnership with a Belgian startup to develop biostimulants. Biologicals’ sales by Bayer amounted to US$214 million in 2022, while in 2023, Corteva reported US$420 million in sales and Syngenta US$400 million.

The top pesticide companies clearly state that their biological products are not meant to replace “traditional crop protection products” but, rather, to be used alongside them. Moreover, while the companies describe their biologicals as “natural products”, this can be misleading because the label is ambiguous and these products raise biosafety issues and can involve genetically modified microorganisms.

Biologicals are part of a larger move by the top pesticide and seed corporations into what they call “regenerative agriculture”. This refers to a vaguely defined set of practices that can also include cover cropping, reduced tillage, crop rotation, genetically modified seeds, biologicals, and digital agriculture. Corporations claim, without convincing scientific evidence, that their model of regenerative agriculture will sequester carbon into soils, among other benefits.

36 Corporate regenerative agriculture programmes ensure companies the extraction of valuable agricultural data from farmers, giving them a competitive advantage in the market.

37 The carbon credits generated by farmers are bought by companies that wish to continue their polluting operations and not reduce their greenhouse gas emissions.

Bayer sees a US$100 billion opportunity in the shift to regenerative agriculture through biologicals, agrofuels, digital agriculture and carbon farming. The growing focus on regenerative agriculture is driving collaborations and partnerships across the industrial food chain. While Syngenta has partnered with Pepsico, McDonalds and Lopez Foods to promote regenerative agriculture, BASF has initiated a project to assess the feasibility of a ‘nature-market’ among soybean farmers in Brazil.

Digital technologies are central to corporate regenerative agriculture programmes. To derive commercial benefits from those, presumed impacts like reduced greenhouse gases and carbon sequestered in soils need to be measured at scale using digital tools. The top seed and agrochemical companies have their own proprietary digital platforms via which they obtain publicly available agricultural data, data from satellites, sensors, farm equipment, data from their own R&D wings and data that farmers share with these platforms. In the case of Bayer, it extracts data from more than 89 million hectares across 20 countries that are subscribed to its Climate FieldView platform. Syngenta’s digital platform covers about 88 million hectares across the world. The top agribusiness companies’ digital agriculture technologies are inextricably linked to Big Tech’s cloud servers and databases.

The digital technologies that Big Ag are rolling out “assist” farmers in deciding when to plant their seeds, what type of seeds to use, how much and what kind of pesticides to spray. They claim to be able to predict disease outbreaks, measure soil health and even estimate yields. Farmers who are enrolled in these programmes have to adopt specific agricultural practices to be eligible to earn money from the production of carbon credits. These digital platforms allow corporations to effectively dictate agricultural practices and push their products on millions of hectares across the world.

Table 2. Top 10 corporations in the pesticides sector

|

Ranking

|

Company (Headquarters)

|

Sales in 2023

(US$ millions)

|

% Global market share

|

|

1

|

Syngenta (China/Switzerland)

|

20,066

|

25

|

|

2

|

Bayer (Germany)

|

11,860

|

15

|

|

3

|

BASF (Germany)

|

8,793

|

11

|

|

4

|

Corteva (US)

|

7,754

|

10

|

|

|

Total top 4

|

48,472

|

61

|

|

5

|

UPL (India)

|

5,925

|

8

|

|

6

|

FMC (Germany)

|

4,487

|

6

|

|

7

|

Sumitomo (Japan)

|

3,824

|

5

|

|

8

|

Nufarm (Australia)

|

2,056

|

3

|

|

9

|

Rainbow Agro (China)

|

1,623

|

2

|

|

10

|

Jiangsu Yangnong Chemical Co., Ltd. (China)

|

1,595

|

2

|

|

|

Total top 10

|

67,982

|

86

|

|

|

Total world market

|

79,000

|

100

|

Another emerging set of alliances in this sector is between commodity trading corporations and fossil fuel companies. For example, Corteva has a partnership to develop canola hybrids for agrofuels with Chevron, the multinational oil and gas company, and Bunge, one of the world’s largest commodity trading corporations. Corteva also has a joint venture with the UK oil company BP that will contract farmers in Europe and the Americas to grow mustard seed, sunflower and canola feedstocks for agrofuels for aviation. In another example, Syngenta is collaborating with the US commodity trader ADM on research and commercialisation of low carbon-intensity oilseeds for agrofuels.

Synthetic fertilisers

Industrial agriculture is highly dependent on synthetic fertilisers. They are differentiated by the type of nutrient they contain: nitrogen in the form of urea, phosphorus (as phosphate) and potassium (as potash). These nutrients (and the fossil fuels used for nitrogen fertiliser production) are globally traded commodities, making the sector particularly vulnerable to price fluctuations and trade disruptions.56

Industrial agriculture is highly dependent on synthetic fertilisers. They are differentiated by the type of nutrient they contain: nitrogen in the form of urea, phosphorus (as phosphate) and potassium (as potash). These nutrients (and the fossil fuels used for nitrogen fertiliser production) are globally traded commodities, making the sector particularly vulnerable to price fluctuations and trade disruptions.56With a market value of US$196 billion, fertilisers is one of the most profitable sectors across the industrial food system, particularly at times of food price spikes.

57 The revenues of the top 10 companies were US$76 billion in 2023 (

see Table 3), an increase of 57% compared to 2020.

58 And in 2022 they had been even higher, 130% more than in 2020.

59 The World Bank explained the spike in fertiliser prices as a result of high natural gas prices from trade disruptions.

60 But a study of Nutrien, Yara, Mosaic, ICL Group, CF Industries, OCP, PhosAgro, OCI and K+S found that they had generated these extreme profits in 2022 by taking advantage of the war in Ukraine raising prices above the increased cost of producing goods, and deepening the debt of farmers and entire countries as a result.

61The global fertiliser market is dominated by a small number of companies, and fertiliser production takes place in a small number of countries. Over 55% of global urea production occurs in four countries: China, India, Russia and the US. And only China, Russia, Saudi Arabia and Qatar account for 41% of nitrogen fertiliser exports. For phosphate fertilisers, 70% of world production and 61% of world exports are concentrated in China, Morocco, the US and Russia. Similarly, for potash fertilisers, Canada, Russia, Belarus and China account for 75% of world production and the first three alone are responsible for 77% of world exports.

62 Many of the top fertiliser companies are based in these producer countries.

At a global level, the top 10 controls 39% of the total market. But this concentration increases when the market is considered by type of fertiliser or by country. For example, five companies, OCP (Morocco), Mosaic (US), ICL (Israel), Nutrien (US) and Sinofert (China) account for a quarter of the phosphate-based fertilisers market.

63 But in the US, Mosaic controls 60% of domestic phosphate fertiliser production and until recently 90% of the domestic market.

64 With potash fertiliser, just four companies– Nutrien, Mosaic, ICL and K+S– occupy 50% of the global market.

65Fertilisers are a leading source of greenhouse gas emissions in the agriculture sector. Nitrogen fertilisers alone are responsible for one in every 40 tonnes of total global emissions each year.

66 There is thus growing international interest in reducing fertiliser use and, in response, the fertiliser companies are ramping up their greenwashing efforts. Like the pesticide companies, the fertiliser companies are investing in biofertilisers and biostimulants, and marketing these as “complementary” to their synthetic fertilisers, often through their digital platforms and carbon credit schemes.

67 Yara, for instance, which recently acquired the Italian organic-based fertiliser company Agribios, has a digital carbon farming platform called Agoro Carbon that is used by farmers on over 809,000 hectares in the US.

68Yara and other fertiliser companies maintain that “green” energies can be utilised to produce nitrogen fertilisers, and thereby dramatically reduce emissions. Their main focus is on blue hydrogen, which is produced from fossil fuels but with carbon capture and storage (CCS), and on green hydrogen, which is produced using wind or solar energy. This is already opening up new markets, such as the inclusion of Yara’s “low-carbon” fertilisers in PepsiCo’s planned 2.8 million hectare regenerative agriculture projects in Latin America.

69 But there is growing criticism of the social and environmental conflicts associated with CCS projects, as illustrated by the case of the residents of Ingleside in the US who are opposing a plant planned by Yara.

70 And while the production of green hydrogen-based fertilisers is lower in its CO

2 emissions, nitrogen oxide emissions still occur on farms. Green hydrogen projects are also increasingly linked to land, water and energy grabs in the Global South.

Table 3. Top 10 corporations in the synthetic fertilisers sector

|

Ranking

|

Company (Headquarters)

|

Sales in 2023

(US$ millions)

|

% Global market share

|

|

1

|

Nutrien (Canada)

|

15,673

|

8

|

|

2

|

The Mosaic Company (US)

|

12,782

|

7

|

|

3

|

Yara (Norway)

|

11,688

|

6

|

|

4

|

CF Industries Holdings, Inc, (US)

|

6,631

|

3

|

|

|

Total top 4

|

46,774

|

24

|

|

5

|

ICL Group Ltd. (Israel)

|

6,294

|

3

|

|

6

|

OCP (Morocco)

|

5,967

|

3

|

|

7

|

PhosAgro (Russia)

|

4,989

|

3

|

|

8

|

MCC EuroChem Joint Stock Company (EuroChem) (Switzerland/Russia)

|

4,298

|

2

|

|

9

|

OCI (Netherlands)

|

4,188

|

2

|

|

10

|

Uralkali (Russia)

|

3,497

|

2

|

|

|

Total top 10

|

76,007

|

39

|

|

|

Total world market

|

196,000

|

100

|

Farm machinery

Farm machinery here refers to manufactured equipment used in agriculture like tractors, haying and harvesting machinery and equipment used for planting, fertilising, ploughing, cultivating, irrigating and spraying. As farm equipment companies move towards digitalisation and automation, this sector can also include their proprietary digital platforms, drones, and robotic technologies.

Farm machinery here refers to manufactured equipment used in agriculture like tractors, haying and harvesting machinery and equipment used for planting, fertilising, ploughing, cultivating, irrigating and spraying. As farm equipment companies move towards digitalisation and automation, this sector can also include their proprietary digital platforms, drones, and robotic technologies.In the farm machinery sector, the top four companies control 43% of the global market according to 2023 sales figures (see Table 4). Much of the focus of these companies is now on integrating AI and digital technologies – through partnerships and acquisitions – to allow for more precision, as they claim, in the application of seeds, pesticides and fertilisers.

In 2023, for example, John Deere acquired Smart Apply, a US precision spraying equipment company. It is developing a technology to reduce indiscriminate agrochemical spraying in vineyards, orchards and nurseries by sensing the size and foliage of individual plants and adjusting the agrochemical volume to be sprayed. But while doing that, the technology will collect valuable on-farm data on pesticide application, canopy volumes, the number of trees, the health of individual trees, and other information to assess the profitability and productivity of the orchard or vineyard. Another technology John Deere is deploying, called See & Spray, uses cameras to detect weeds in farms. The company says this technology saved farmers from spraying approximately 8 million gallons of herbicide across over 400,000 hectares in 2024. See & Spray is being utilised in a partnership John Deere has with Syngenta and the US-based company InnerPlant to develop genetically modified “sensor plants” (like cotton, soybeans and maize). The GM plants will send out signals when stressed by drought, pests or fertiliser deficiencies which would then be detected by See & Spray and then treated with Syngenta’s pesticides. Innerplant calls it “the most exciting GM trait since Roundup Ready”.

Syngenta also has a partnership with CNH Industrial to integrate its digital farming platform Cropwise with CNH’s farm machinery. This will likely give both corporations seamless access to the data accumulated by each other giving CNH access to Syngenta’s valuable on-farm data and Syngenta the opportunity to promote its products through CNH.

The farm machinery giants are also positioning their technologies to be part of regenerative agriculture and carbon farming programmes. John Deere, for instance, is partnering with Cargill’s regenerative agriculture programme RegenConnect to collect data on agricultural practices from farms, analyse if they fulfil Cargill’s sustainability criteria, and, eventually, buy and commercialise carbon credits. Another example is the partnership between Kubota and Tokyo Gas to reduce methane emissions from rice cultivation in the Philippines. Under the project, Filipino farmers are told how to select seeds, manage soil and implement a rice-growing technique to reduce methane emissions, with the companies extracting data to create carbon credits for Kubota and Tokyo Gas.

Since the new machinery technologies under development require farms to have a high-speed internet connection, the farm machinery companies are partnering with telecom and satellite giants to expand rural internet connectivity. CNH, for example, is partnering with Telecom Argentina to expand internet connectivity across 500,000 hectares in Buenos Aires, while John Deere has a partnership with Elon Musk’s SpaceX satellite telecommunications company.

Table 4. Top 10 corporations in the farm machinery sector

|

Ranking

|

Company (Headquarters)

|

Sales in 2023

(US$ millions)

|

% Global market share

|

|

1

|

Deere and Co. (US)

|

26,790

|

15

|

|

2

|

CNH Industrial (UK/Netherlands)

|

18,148

|

10

|

|

4

|

AGCO (US)

|

14,412

|

8

|

|

3

|

Kubota (Japan)

|

14,233

|

8

|

|

|

Total top 4

|

73,583

|

43

|

|

5

|

CLAAS (Germany)

|

6,561

|

4

|

|

6

|

Mahindra and Mahindra (India)

|

3,156

|

2

|

|

7

|

SDF Group (Italy)

|

2,197

|

1

|

|

8

|

Kuhn Group (Switzerland)

|

1,583

|

0.9

|

|

9

|

YTO Group (China)

|

1,493

|

0.9

|

|

10

|

Iseki Group (Japan)

|

1,057

|

0.6

|

|

|

Total top 10

|

89,629

|

52

|

|

|

Total world market

|

173,000

|

100

|

Animal pharma

The animal pharmaceutical industry includes medicines and vaccines, diagnostics, medical services, nutritional supplements (medicated feed additives), veterinary and other related services for animal health.

The animal pharmaceutical industry includes medicines and vaccines, diagnostics, medical services, nutritional supplements (medicated feed additives), veterinary and other related services for animal health.According to some estimates, global animal pharmaceutical sales totalled US$48 billion in 2023.

100 The main markets are the US (42.3%) and Europe (27.3%), where the largest companies in the sector are based.

101 In 2023, the top 10 controlled 68% of the market, with the top four companies accounting for almost half of all sales (

see Table 5).

Most animal pharma revenues are generated from pets, not livestock. In 2023, livestock accounted for 45.8% of the animal pharma market, down from 59% in 2020.

102 But this varies by country. For example, in 2023, Zoetis’ products for pets accounted for 80% of 2023 sales in the US, 70% in Japan and 69% in China, while in Brazil, livestock products represented 59% of its sales.

103Pets’ health has attracted players from other sectors, such as the US based Mars Inc., one of the world’s largest food companies. The corporation has been increasing its investment in the veterinary sector, and currently owns 3,000 veterinary clinics worldwide.

104 As it is a private company, its revenues are not made public, but according to Mars, 60% of its US$50 billion in sales in 2023 came from the Mars Petcare segment, which includes pet food and veterinary care.

105 Nearly half of Mars’ 150,000 workers are with its Mars Veterinary Health division.

106 The large retailer Walmart is also moving into this sector, building veterinary clinics inside its US stores.

107Corporate concentration in this sector gives companies the power to exert strong pressure on governments to influence legislation in problematic sectors such as antibiotics. The global sales of farm antibiotics is valued at US$5.10 billion, with cattle accounting for near 40% of the use.

108 For years, the industry has defended the use of antibiotics in farm animals by linking them to faster growth, better health, and “feed efficiency”.

109 The problem, however, is that use of antibiotics in animals can lead to the emergence of bacteria that are resistant to antibiotics, including those critical to human health. Antibiotic resistance is already responsible for the deaths of 700,000 people around the world every year.

110 Despite strong opposition from Elanco, Zoetis, Phibro and others, the European Union managed to reduce the overuse of antibiotics on farms, but widespread use continues in the US and elsewhere.

111As industrial livestock is a major source of greenhouse gas emissions, accounting for 14.5% of total emissions according to the IPCC, animal pharma companies are trying to show they are taking climate action by developing drugs that can reduce emissions.

112 Elanco, for example, has won approval in the United States to market the drug Experior which claims to reduce ammonia gas in cattle.

113 However, such techno-fixes can have only marginal overall impact, as livestock emissions occur across the whole industrial chain, from deforestation for feed crops, manure lagoons, to waste, to the use of fossil fuels throughout the production process.

114Table 5. Top 10 corporations in the animal pharma sector

|

Ranking

|

Company (Headquarters)

|

Sales in 2023

(US$ millions)

|

% Global market share

|

|

1

|

Zoetis (US)

|

8,544

|

18

|

|

2

|

Merck & Co (MSD) (US)

|

5,625

|

12

|

|

3

|

Boehringer Ingelheim Animal Health (Germany)

|

5,100

|

11

|

|

4

|

Elanco (US)

|

4,417

|

9

|

|

|

Total top 4

|

23,686

|

49

|

|

5

|

Idexx Laboratories (US)

|

3,474

|

7

|

|

6

|

Ceva Santé Animale (France)

|

1,752

|

4

|

|

7

|

Virbac (France)

|

1,348

|

3

|

|

8

|

Phibro Animal Health Corporation (US)

|

978

|

2

|

|

9

|

Dechra (UK)

|

917

|

2

|

|

10

|

Vetoquinol (France)

|

572

|

1

|

|

|

Total top 10

|

32,727

|

68

|

|

|

Total world market

|

48,000

|

100

|

Livestock genetics

The genetic material used in the industrial production of meat, dairy and aquaculture is supplied by a small number of relatively unknown companies that are mostly privately owned. As detailed financial data is not publicly available for most of these companies, it is difficult to determine companies’ market shares and even the value of the global market. However, it was possible to arrive at some estimates for chicken, which tops global meat production (narrowly exceeding pigs).

126Corporate concentration is particularly acute with chicken. Just three companies dominate the poultry genetics market: Tyson Foods (US, public), EW Group (Germany, private) and Hendrix Genetics (Netherlands, private). Together, they supply more than 120 countries with breeds through licensing and distribution agreements or through their own farming operations.

127Tyson and EW Group control the two main hybrid breeds used in most of the world’s industrial broiler farms (chickens for meat): Cobb (Cobb-Vantress) and Ross (Aviagen).

128 While Tyson does not provide a breakdown of sales from its genetics division, EW Group subsidiaries Aviagen Limited (UK) and Hubbard S.A.S reported sales of $252 million and $68 million respectively in 2023.

Both Tyson and EW Group operate in the US, Brazil and China, where 51% of the world’s chicken production takes place.

130 In the US, they supply the breeding stock for 98% of broilers, with Cobb-Vantress holding half of the market.

131 In Brazil, the Cobb type accounts for 60% and Ross for 35% of all industrial breeds.

132 China is still 70% dependent on imports of chicken genetics, with Cobb-Vantress and Aviagen breeding half of the domestic grandparent stock locally.

133 But the Chinese state and Chinese companies are working to break this dependency, particularly in light of the outbreaks of bird flu in the US. Three local companies, Sunner Group, Yukou Poultry and Xinguang Nongmu, now have nearly 30% of the market, with Sunner holding over 20%.

134 They have also started to export to countries such as Tanzania, Pakistan and Uzbekistan.

Global companies in the sector are looking at the African market for growth, where, in many countries, indigenous chickens still account for 80% or more of the chicken population.

136 In southern and eastern Africa, Tyson and EW Group’s Aviagen have merged with regional partners over the past decade, including cross-shareholdings. Some of the joint ventures are through companies registered in the tax haven of Mauritius.

137 In Zambia, which is increasingly used as a hub for chicken exports to the region, Tyson and EW Group dominate the entire market, holding 45% and 55% market shares, respectively. Zambian regulators found in 2018 that the genetics companies were coordinating to restrict the supply of breeding stock and increase prices, thus affecting smaller producers and consumers. Similar behaviour was found in the US, resulting in fines.

138EW Group is also the top player in sales of genetics for chickens used for laying eggs (layer), through its subsidiaries Hy-Line International and Novogen S.A.S.

139 Second is Hendrix Genetics, owned by private equity firm Paine Schwartz Partners, with layer genetics sales estimated at US$274 million in 2023.

140 China is the main producer of eggs with 34% of global egg production, followed by the US, India and Indonesia with 7% each.

141 Chinese reliance on imported grandparent layer breeders is also decreasing and is currently below 30%, but EW Group and Hendrix Genetics still supply genetics to several of China’s largest egg producing companies.

142 In the US, EW Group and Hendrix Genetics not only have a monopoly on layer genetics, but also dominate the layer supply chain, through their control of hatcheries. In the recent ‘egg crisis’ that hit the country, there were allegations that the two companies colluded with dominant egg producers to keep prices high.

143The focus on uniformity, scale and high yields makes the breeds of these companies highly susceptible to diseases. Even with strict biosecurity measures on farms, disease outbreaks still occur, as can be seen in the massive number of outbreaks of bird flu at industrial farms in the US and Europe in 2024 and 2025. In response, genetics companies are trying to breed chickens resistant to bird flu and other diseases using gene editing techniques, like CRISPR-Cas9.

144 For example, Cobb-Vantress co-funded research into the use of CRISPR to create chickens resistant to avian flu, which showed that multiple genetic modifications were needed to prevent “viral escape”.

145 Companies are also genetically modifying chickens for increased growth rates and sex sorting.

Illustrations: Andre M. Medina (@andre_m_medina)

Notes:

For an understanding of the history of corporate concentration in the seed, pesticide, fertiliser and agricultural machinery sectors, see Jennifer Clapp, “Titans of Industrial Agriculture. How a few giant corporations came to dominate the farm sectors and why it matters”, Massachusetts Institute of Technology, Cambridge, Massachusetts, 2025.

5Attempts towards mergers and acquisitions across the industrial food chain, like in commodity trading sectors, grocery retail, and food and beverage processing corporations continue full throttle. See: Bunge, “Bunge Shareholders Approve Viterra Combination”, 5 October 2023,

https://www.bunge.com/Press-Releases/Bunge-shareholders-approve-viterra-merger; Jody Godoy, “Kroger’s $25-billion deal for grocery rival Albertsons blocked by US courts”, Reuters, 11 December 2024,

https://www.reuters.com/legal/us-court-blocks-krogers-25-billion-acquisition-grocery-rival-albertsons-2024-12-10/; and Mars, “Mars to Acquire Kellanova”, 14 August, 2024,

https://www.mars.com/en-in/news-and-stories/press-releases-statements/mars-acquisition-august-2024

8See: Corporate Europe Observatory, “Yara: Poisoning our soils, burning our planet,” 17 September 2019,

https://corporateeurope.org/en/2019/09/yara-poisoning-our-soils-burning-our-planet; Corporate Europe Observatory, “Monsanto lobbying: an attack on us, our planet and democracy,” Undated,

https://corporateeurope.org/sites/default/files/attachments/monsanto_v09_web.pdf; and Peter Waldman, Tiffany Stecker, and Joel Rosenblat, “ Monsanto was its own ghostwriter for some safety reviews”, Bloomberg, 9 August 2017,

https://www.bloomberg.com/news/articles/2017-08-09/monsanto-was-its-own-ghostwriter-for-some-safety-reviews

11In this report, commas are used to separate thousands. Dots are used to separate decimals.

13See: Chris Westfall, “Cutting middle management: Bayer’s costly experiment one year later”, 7 January 2025, Forbes,

https://www.forbes.com/sites/chriswestfall/2025/01/07/cutting-middle-management-bayers-costly-experiment-one-year-later/; Anonymous, “‘Broken’ Bayer needs bolder action”, Financial Times, 7 March 2024,

https://www.ft.com/content/c1d9b0a6-2c25-4184-9a92-6d4ea13546bc; Bayer Annual report 2024, p. 2,

https://www.bayer.com/sites/default/files/2025-03/bayer-annual-report-2024.pdf

19Percentages in the figure indicate the shares in the total, and may not tally due to rounding.

42See:

Hope Shand, Kathy Jo Wetter and Kavya Chowdhry, “Food Barons 2022: crisis profiteering, digitalization and shifting power”, ETC Group, September 2022, https://www.etcgroup.org/files/files/food-barons-2022-full_sectors-final_16_sept.pdf; ETC Group, “Behind sugar and spice and everything nice”, 9 May 2024,

https://etcgroup.org/content/behind-sugar-and-spice-and-everything-nice; GRAIN, “Techno feudalism takes root on the farm in India and China”, 24 October 2024,

https://grain.org/e/7196

58Sinofert (China) and K+S (Germany) are not included in the table, but their revenues in 2023 (US$3,070 million and US$2,943 million respectively) are not far behind Uralkali (see: Sinofert Holdings Limited Annual report 2023”,

https://www.hkexnews.hk/listedco/listconews/sehk/2024/0425/2024042502498.pdf; and K+S Annual report 2023, p.58,

https://www.kpluss.com/.downloads/ir/2024/kpluss-annual-report-2023.pdf). For the figures for 2020, see: Hope Shand, Kathy Jo Wetter and Kavya Chowdhry, “Food Barons 2022: crisis profiteering, digitalization and shifting power”, ETC Group, September 2022,

https://www.etcgroup.org/files/files/food-barons-2022-full_sectors-final_16_sept.pdf

59Source: Companies’ annual reports 2023 and Capital IQ.

64As Jennifer Clapp explains, Mosaic deployed a strong lobbying effort in order the US imposes tariffs on fertiliser imports from Morocco and Russia in 2017. This gave Mosaic control over 90% of the phosphate fertiliser market. In 2023, the US lowered tariffs on Moroccan fertilisers and raised those on Russian phosphate fertilisers (See: Jennifer Clapp, “Titans of industrial agriculture. How a few giant corporations came to dominate the farm sectors and why it matters”, Massachusetts Institute of Technology, Cambridge, Massachusetts, 2025.

67See: Jennifer Clapp, “Titans of industrial agriculture. How a few giant corporations came to dominate the farm sectors and why it matters”, Massachusetts Institute of Technology, Cambridge, Massachusetts, 2025; and GRAIN, “Regenerative agriculture was a good idea, until corporations got hold of it”, 1 December 2023,

https://grain.org/e/7067

72Nutrien Annual report 2023,

https://www.nutrien.com/investors/financial-reporting. Includes: retail crop nutrients value (US$ 8,379 million, p. 52), nitrogen fertilisers value (US$ 2,450 million, p. 58), potash fertiliser value (US$3,759 million, p. 55), and phosphate fertiliser value (US$ 1,085 million, p. 60).

109Mariano Enrique Fernández Miyakawa, Natalia Andrea Casanova, and Michael H. Kogut, “How did antibiotic growth promoters increase growth and feed efficiency in poultry?”, Poultry Science, Vol. 103, Issue 2, 2024,

https://doi.org/10.1016/j.psj.2023.103278.

128See: Sumayya Goga, Simon Roberts, “Multinationals and competition in poultry value chains in South Africa, Zambia, and Malawi”, August 2023,

https://www.researchgate.net/publication/375864070; Dani Sher, “Broiler chickens: Who are they and how long do they live?”, Farm Forward, 13 March 2023,

https://www.farmforward.com/news/broiler-chickens/ ; and Simon Usborne, “The £3 chicken: how much should we actually be paying for the nation’s favourite meat?”, The Guardian, 24 November 2021,

https://www.theguardian.com/food/2021/nov/24/the-3-chicken-how-much-should-we-actually-be-paying-for-the-nations-favourite-meat

129Source: Capital IQ. Hubbard S.A.S is a subsidiary of Aviagen Group Holding, Inc.

139Hy-Line International’s revenue for 2023 is not available, but Novogen reported US$14 million (Capital IQ).

145Idoko-Akoh, A., Goldhill, D.H., Sheppard, C.M. et al. “Creating resistance to avian influenza infection through genome editing of the ANP32 gene family”. Nat Commun 14, 6136 (2023),

https://doi.org/10.1038/s41467-023-41476-3

The genetic material used in the industrial production of meat, dairy and aquaculture is supplied by a small number of relatively unknown companies that are mostly privately owned. As detailed financial data is not publicly available for most of these companies, it is difficult to determine companies’ market shares and even the value of the global market. However, it was possible to arrive at some estimates for chicken, which tops global meat production (narrowly exceeding pigs).126

The genetic material used in the industrial production of meat, dairy and aquaculture is supplied by a small number of relatively unknown companies that are mostly privately owned. As detailed financial data is not publicly available for most of these companies, it is difficult to determine companies’ market shares and even the value of the global market. However, it was possible to arrive at some estimates for chicken, which tops global meat production (narrowly exceeding pigs).126

CORPORATE AGRIBUSINESS GIANTS SWIM IN WEALTH AS MORE POOR PEOPLE GO HUNGRY AMID THE BITING COVID PANDEMIC.

CORPORATE AGRIBUSINESS GIANTS SWIM IN WEALTH AS MORE POOR PEOPLE GO HUNGRY AMID THE BITING COVID PANDEMIC.

A corporate cartel fertilises food inflation

A corporate cartel fertilises food inflation

The United Nations Food Systems Summit is a corporate food summit —not a “people’s” food summit

The United Nations Food Systems Summit is a corporate food summit —not a “people’s” food summit

Food inflation: The math doesn’t add up without factoring in corporate power

Food inflation: The math doesn’t add up without factoring in corporate power

Activists storm TotalEnergies’ office ahead of G20 Summit, demand end to fossil fuel expansion in Africa

Activists storm TotalEnergies’ office ahead of G20 Summit, demand end to fossil fuel expansion in Africa

New billion-dollar loans to fossil fuel companies from SEB, Nordea and Danske Bank.

New billion-dollar loans to fossil fuel companies from SEB, Nordea and Danske Bank.

Fossil fuel opponents lobby Africans for support

Fossil fuel opponents lobby Africans for support

Ecological land grab: food vs fuel vs forests

Ecological land grab: food vs fuel vs forests

Uganda, Total sign crude oil pipeline deal

Uganda, Total sign crude oil pipeline deal

Witness Radio – Uganda, Community members from Mozambique and other organizations around the world say NO to more industrial tree plantations

Witness Radio – Uganda, Community members from Mozambique and other organizations around the world say NO to more industrial tree plantations

NGOs file suit against Total over Uganda oil project

NGOs file suit against Total over Uganda oil project

Agribusiness Company with financial support from UK, US and Netherlands is dispossessing thousands.

Agribusiness Company with financial support from UK, US and Netherlands is dispossessing thousands.

Victims of human rights violations in Uganda still waiting for redress

Victims of human rights violations in Uganda still waiting for redress

Business, UN, Govt & Civil Society urge EU to protect sustainability due diligence framework

Business, UN, Govt & Civil Society urge EU to protect sustainability due diligence framework

Development financiers fuel human rights abuses – New Report

Development financiers fuel human rights abuses – New Report

FARM NEWS2 weeks ago

FARM NEWS2 weeks ago